Tuesday, October 5, 2021

The debt limit—commonly called the debt ceiling—is the maximum amount of debt that the Treasury Department can issue to pay its already committed financial obligations. The amount is set through Congress and has been increased 78 times since 1960. Through a bipartisan budget act in 2019 however, Congress suspended the debt ceiling through July 31, 2021. Since August 1, Treasury department officials have essentially shuffled funds around to meet the nation’s payment obligations—but Treasury Secretary Janet Yellen says the department will no longer be able to pay all of its debts when they come due on or shortly after October 18.

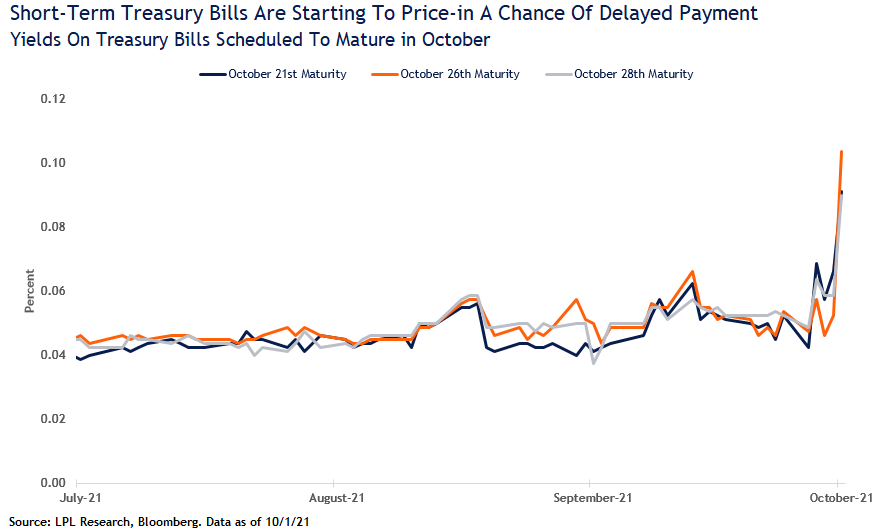

“Our base case is that Congress will do the right thing and raise or suspend the debt ceiling in time,” noted LPL Financial Fixed Income Strategist Lawrence Gillum. “However, the longer they wait, the more unnecessary volatility we’ll likely see in markets.”

If the debt ceiling isn’t resolved, the U.S. Government would technically default on its contractual obligations. As seen in the LPL Research Chart of the Day, bond markets are starting to price in, however remote, a chance of delayed payment. Yields on debt maturing after October 18 have started to move higher as they are the securities most at risk of delayed payment. As we get further into October, unless resolved, we could see yields on additional short-maturity Treasury bills move higher still as the prospects of non-repayment, however slight, get further priced into the market.

At this point, there are two traditional ways Congress could raise/suspend the debt ceiling- through a bipartisan vote or through budget reconciliation. A bipartisan vote, which would need 60 votes in the Senate and thus 10 Republicans to vote with Democrats, seems unlikely given the reluctance of Senate Republicans to vote for an increase in the debt ceiling. The more likely scenario is that the debt ceiling is raised or suspended through the budget reconciliation process, which only requires 51 votes so the Democrats can go at it alone. There has been a general reluctance from Democratic leadership to go this way but it is increasingly likely the only realistic way to stave off a technical default.

Other, less tested options, include the Treasury minting a trillion-dollar platinum coin or through the Public Debt Clause found in the 14th Amendment, which some have interpreted to allow the Treasury to continue to issue debt to prevent default. Yellen has recently commented that both of those options are currently unworkable and both would likely be tied up in the courts for some time.

U.S. bond market investors have taken for granted the government’s ability and willingness to pay its debt. While its ability to repay its obligations is not in question, the debt ceiling debate complicates the country’s willingness to pay its debts. In 2011, Congress waited until the very last minute to fix the debt ceiling issues and S&P downgraded the country’s debt rating to AA+ from AAA because of the questions surrounding that willingness to pay its obligations. Now, another rating agency, Fitch, has threatened to do something similar if Congress fails to act soon. Another debt downgrade would likely be disruptive to financial markets. While we think Congress will act in time and either raise or suspend the debt ceiling, these games of political chicken can introduce volatility to markets in the meantime.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from FactSet and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking # 1-05198035