Monday, February 28, 2022

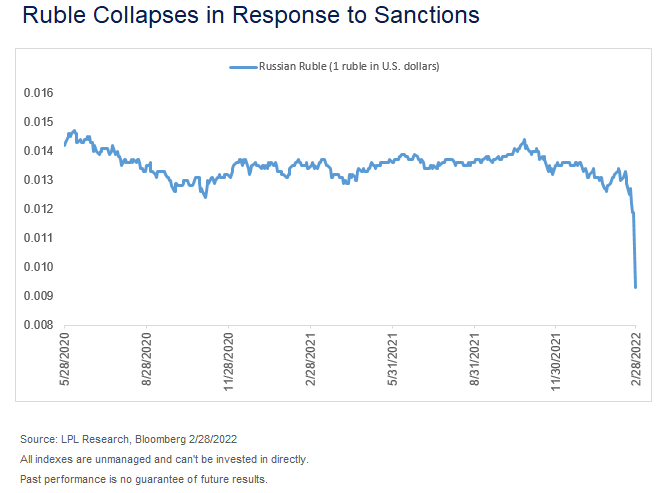

After weeks of intense multilateral diplomacy, the U.S., Canada, the European Union, and the U.K. unleashed powerful economic sanctions against Russia over the weekend that have sent its economy reeling. As shown in the LPL Chart of the Day, the Russian ruble has collapsed in response to the economic pressure, just one sign that the sanctions are working.

“The impact of the sanctions has been both immediate and dramatic, and the pressure will only increase over time,” said LPL Financial Asset Allocation Strategist Barry Gilbert. “There may be some broader economic damage from the conflict via more protracted inflation, tighter financial conditions, and some drag on global growth. It’s a fluid situation but we think fundamentals remain strong enough to support a rebound in equities.”

Here are 6 key things to know about the sanctions and their potential impact on financial markets:

- The sanctions took two main forms. On Saturday the U.S. and its allies announced they would cut Russia’s most important banks off from SWIFT, a secure messaging system that facilitates most international transactions. While this would apply considerable financial pressure, Russia has put together a vast war chest of about $630 billion in foreign exchange reserves over the years to help insulate itself from sanctions. But the U.S. and its allies have announced that they are also cutting Russia’s central bank off from international markets, severly limiting Russian’s ability to respond to the sanctions.

- The sanctions’ bite was immediately felt, with offshore trades in the Russian ruble declining sharply, a downgrade of Russian debt by one rating agency from investment grade to junk status, and lines forming at Russian ATMs to withdraw currency.

- The economic pressure will likely push Russia toward recession and will put considerable pressure on the stability of the Russian banking system.

- In an extreme move, the Russian central bank increased its key interest rate to 20% from 9.5%, in an attempt to support the ruble. This is now above the 17% last seen when Russia illegally annexed Crimea from Ukraine in 2014. Authorities also told export-focused companies to be ready to sell foreign currency to support the ruble.

- Corporations are initiating restrictions as well. BP, United Parcel Services, and FedEx have either cut or limited exposure to Russia, with many more expected to follow suit.

- The sanctions have also put pressure on dollar funding markets and central banks may need to step in to help provide liquidity. The European Central Bank (ECB) governing council is meeting on March 10 and will likely communicate a less hawkish stance as rising risks from the East could put a damper on western Europe’s growth path. Although the U.S. will likely feel less ripple effects from Russia, the Fed will be less likely to “shock and awe” the market with an overly aggressive hike on March 15-16.

Our main market takeaways:

- The energy sector is a beneficiary of the conflict, with WTI Crude approaching $100 per barrel and the U.S. poised to fill some of the Russian supply gap.

- Europe, with its heavy dependence on Russian energy supplies, is taking on the most risk with sanctions. Germany may be entering a recession due to the added economic pressure. The U.S. dollar is also seeing safe haven flows, weighing on international equity returns.

- Emerging markets are likely to underperform, at least in the short term, on dollar strength and Russian weakness, though Russia only composes about 2% of the MSCI Emerging Markets Index. China may be more resilient.

- Gold may be an effective hedge in this environment despite potential U.S. dollar strength. The technical setup is favorable.

- We continue to recommend an overweight equities allocation given the still-solid U.S. economic and corporate profit backdrop, coupled with low interest rates but volatility is likely to remain high until there is some sort of resolution in Ukraine and inflation moderates.

While a significant step in supporting Ukraine, sanctions do little to directly mitigate the humanitarian crisis on the ground. The hope is the added pressure will shorten the conflict while preserving Ukraine’s national sovereignty and make future conflicts less likely. We’ve been able to see some immediate effects on Day 1 and it’s not something Russian President Vladamir Putin can ignore.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from FactSet and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use –Tracking # 1-05250129