Thursday, October 7, 2021

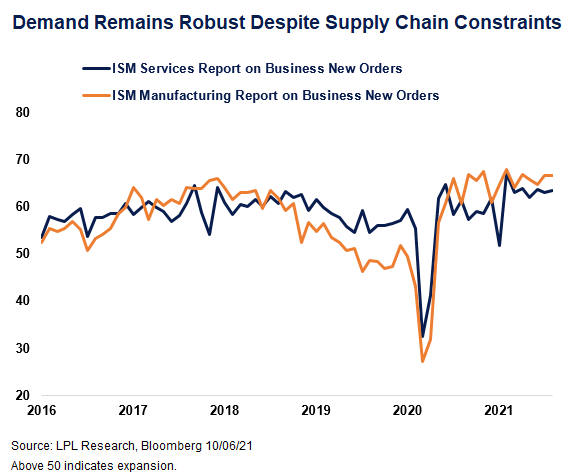

Based on recent readings of manufacturing and service sector activity, business demand remains strong, further damaging the “stagflation” narrative. At the same time, barriers to meeting demand continue to limit businesses’ ability to respond, including ongoing global supply chain disruptions, difficulties hiring, and high prices. As seen in the LPL Chart of the Day, the Services and Manufacturing New Orders Indexes in the Institute for Supply Management’s monthly surveys both posted strong numbers for September and remain elevated. New orders tend to be a leading indicator of future economic activity as orders are met.

“The most recent ISM new orders numbers show an economy still raring to go as we look toward 2022,” said LPL Chief Market Strategist Ryan Detrick. “There’s plenty of pent-up demand, but supply constraints are still in place and it’s going to take time for them to unwind.”

The new orders readings for the manufacturing and service sectors helped support the headline purchasing manager index (PMI) readings in September. The headline numbers came in at 61.1 and 61.9 respectively, both topping economists’ consensus expectation and accelerating from August despite the ongoing impact of the Delta variant. But there were concerns underneath the surface. Price pressures picked up in both indexes and remain elevated. Supplier deliveries remain slow due to supply chain disruptions. The backlog of orders, while improving, remains somewhat elevated as well.

While we do believe these pressures will steadily decrease over the next year, it will be a gradual process. According to the Bloomberg-surveyed economists’ consensus estimate, we’re likely to average around 300,000 new jobs created per month in 2022, and headline inflation is expected to settle back down to around 3%, still elevated but moving in the right direction. Supply chains will probably take a couple of years to be fully addressed, just because of the scale of the problem. Despite challenges around supply chains, hiring, and prices, if the demand is there it will help drive continuous improvement as businesses adapt to address challenges. That is likely to leave us with above-trend economic growth, low recession risk, and a positive economic backdrop for markets for 1-2 more years.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from FactSet and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking #1-05199232