Thursday, October 14, 2021

The U.S. Bureau of Labor Statistics (BLS) released its monthly Job Openings and Labor Turnover Survey (JOLTS) report this week revealing that the number of American workers who are voluntarily quitting their jobs is at its highest rate since the BLS started publishing the data in 2001. While not always true, the most common reason for voluntarily leaving a job is to start a new one.

“More and more people are quitting their jobs as competition for qualified workers heats up,” explained LPL Financial Chief Market Strategist Ryan Detrick. “The tightening labor market is putting upward pressure on wages, as employers try to hang onto current employees or bring in new staff, adding to immediate inflationary pressures in the broader economy.”

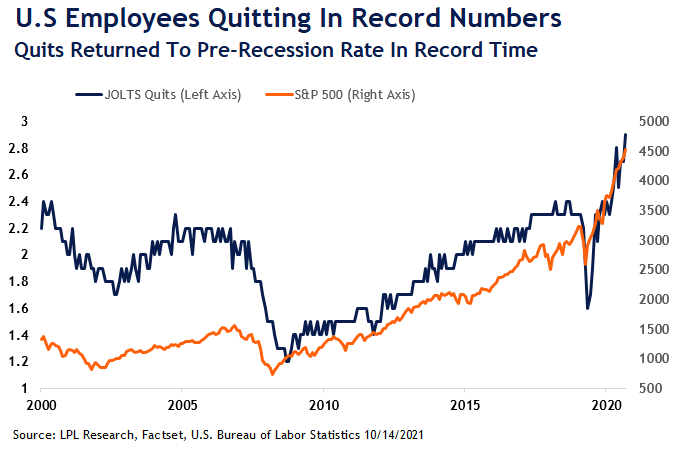

As shown in the LPL Research Chart of the Day, the quit rate for August jumped to 2.9%, equating to 4.3 million people voluntarily leaving their jobs, beating the previous series high of 2.8% that occurred in April of this year.

The rate of employees leaving their jobs voluntarily has been steadily increasing since a series low of 1.2% in September 2009. During the dot com and great financial crisis recessions, the quit rate tended to bottom out around 6 months to a year after the S&P hit its bear market low and the quit rate slowly recovered to near its pre-recession highs, taking 4 and 10 years respectively. The COVID-19 recession has been much accelerated in comparison, with the quit rate bottoming just a month after the S&P 500 and only taking 6 months to get back to its pre-pandemic high.

Some industries in particular are having trouble holding onto staff based on the latest JOLTS data. Accommodation and food services suffered the highest rate at 6.8% (up from 5.6% the prior month and 4.3% a year ago) with retail trade next highest at 4.7% (up from 4.4% last month and 3.4% a year ago.)

There are several reasons for the elevated level of quits, among them people leaving jobs through worries relating to COVID-19, especially in the South and Midwest regions, which had higher Delta variant surges in the summer. Those regions also had higher quit rates, each at 3.2%, compared to 2.7% in the West and only 2.2% in the Northeast. Another factor is that the higher salaries and sign-on bonus incentives appear to be fueling churn of employees between jobs, with understaffed employees left behind suffering from burnout, which in turn increases the chance of more turnover. With U.S. household net worth at record highs, employees also appear to be more confident they have a sufficient safety net to quit jobs for more flexible work schedules, for a better location, or just for work that they think they will find more enjoyable.

The latest September survey data from the National Federation of Independent Businesses (the NFIB) also highlighted issues that businesses are having with staffing. A majority of small business owners, 51%, reported that they had job openings that they could not fill, a record high for the third consecutive month. In addition, 34% of owners reported few qualified candidates for open roles while 28% reported not having any qualified candidates apply. Finally, 42% of owners reported raising compensation costs during September, again a series high in the 48 year-history of the NFIB data.

While the jobs data continues to point to an inflation jump in the short-to-intermediate term, we do believe that longer-term inflation will remain reasonably well contained. Market-based measures can tend to overshoot in both directions based on prevailing sentiment, and we think ultimately that it’s unlikely that inflation remains elevated. Restarting the economy after a recession often creates supply disruptions that feed into inflation, though in time these effects have previously been self-corrected. As mentioned, similar phenomena occurred exiting the prior recessions, albeit on a more elongated timeline. We anticipate in the long term that forces limiting inflation, such as globalization and technology, will prove stronger than the short-term inflationary pressures we are currently experiencing.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from FactSet and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking # 1-05202060