Friday, October 8, 2021

The September payroll report likely created more questions than it answered.

The U.S. Bureau of Labor Statistics released its September employment report this morning, revealing that the domestic economy added a disappointing 194,000 jobs during the month, falling well short of Bloomberg-surveyed economists’ median forecast for a gain of 500,000. This comes on the heels of a lukewarm August report, which did receive an upward revision of 131,000. Somewhat contradictory, the unemployment rate fell more than forecast to 4.8% in September, beating expectations, though that was paired with a reduced labor force participation rate of 61.6% when expectations called for an increase.

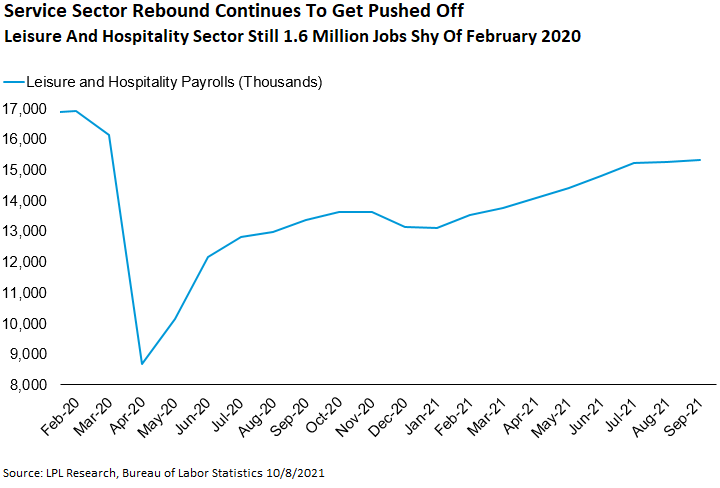

“The observation window for this report likely came too soon for positive catalysts to really gain traction,” explained LPL Financial Chief Market Strategist Ryan Detrick. “Leisure and hospitality jobs, a proxy for economic reopening, were only marginally higher. We take this to mean Delta’s waning impact will likely be more evident in October’s report where we expect to see reopening momentum reassert itself.”

As seen in the LPL Chart of the Day, in-person segments of the labor market such as leisure and hospitality jobs grew steadily during the first half of the year when COVID-19 remained under relative control. However, the latest flare-up has dampened that trend. We expect to see renewed growth in this sector as the delta variant continues to abate.

As mentioned, definitive takeaways from this report are difficult to come by due to the offsetting nature of the report. On the one hand, headline numbers came in very weak, but private payrolls, as well as manufacturing payrolls, fared better. The unemployment rate experienced a significant drop, but interpreting that number becomes muddied when considering the fact that we are already experiencing a significant worker shortage and the participation rate is declining, not increasing, as we would hope to see in a true recovery.

What is more, because the observation window for the report cuts off mid-month, we cannot yet draw conclusions about the impact of school reopening and the lapsing of enhanced unemployment benefits—hotly debated crosscurrents—plus the aforementioned waning delta impact. Regarding the inflation debate—average hourly earnings rose 0.6% month over month and 4.6% year over year. And while wages are undeniably growing and helping to fuel inflation, the data are not mix-adjusted and therefore are inflated due to the suppressed growth in the in-person, lower-wage segment of the labor market.

The biggest question, though, is what this means for the Federal Reserve’s (Fed) asset tapering plans. The market had all but expected the Fed to announce a tapering timeline at its next meeting coming into this report, with the caveat that Fed Chair Jerome Powell needed only to see a “reasonably good” job report first. Whether September’s surprise report has cleared that low bar or not now becomes an open question, one which the market had all but dismissed as a formality previously.

Indeed, in the aftermath of the report’s release Treasury markets immediately began pricing in a possible delay to any taper, and equity markets gyrated between positive and negative territory as they struggled to process whether bad news should actually be considered good news in this context. We will have to see in the coming weeks whether this report will be substantial enough to bring on the much-anticipated taper announcement, but one thing is for sure—there are no gimmies in this labor market recovery.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

If your representative is located at a bank or credit union, please note that the bank/credit union is not registered as a broker-dealer or investment advisor. Registered representatives of LPL may also be employees of the bank/credit union.

These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, the bank/credit union. Securities and insurance offered through LPL or its affiliates are:

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking # 1-05199763