Daily Insights

Stocks opened higher. Reports over the weekend suggested the White House may be able to strike a stimulus deal with the US House Democrats before the election, but the odds are still long, and early 2021 appears more likely. Talks will continue today. European markets are mixed in midday trading. Asian markets finished modestly higher, though generally good Chinese data over the weekend failed to lift Chinese stocks.

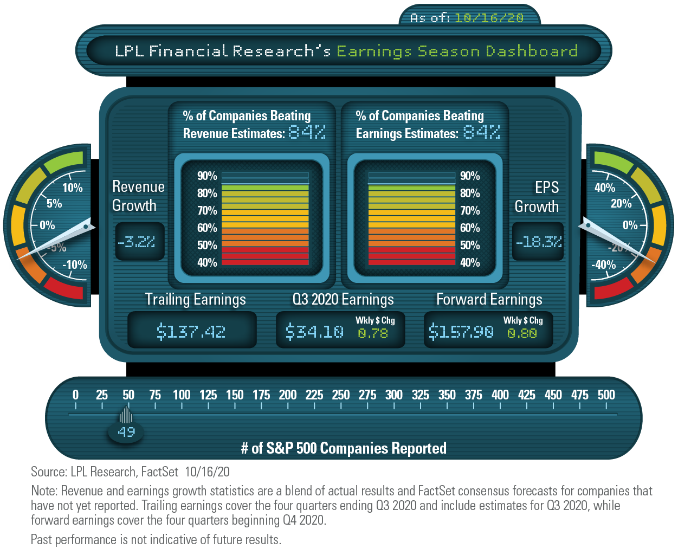

Excellent start to earnings season. With about 10% of S&P 500 Index companies having reported, index earnings for the third quarter are tracking to an 18% year-over-year decline, a big improvement from the more than 30% decline in the second quarter, and 3 percentage points above September 30 estimates. This week 96 S&P 500 companies are slated to report results.

China’s economy posts solid growth. China reported a 4.9% year-over-year increase in gross domestic product for its third quarter, attributable to the fact that the country had contained the virus first after being its origin. China’s impressive growth—including recovering all lost output from the first half of the year—is a key reason for our positive view of emerging markets, in addition to our expectation of a weaker US dollar and attractive valuations.

Week ahead. In addition to a barrage of earnings reports, this week’s economic calendar includes:

- National Association of Home Builders (NAHB) Housing Market Index on Monday

- Building permits and housing starts on Tuesday

- Federal Reserve (Fed) Beige Book on Wednesday

- Jobless claims and leading indicators on Thursday

- US Purchasing Manager’s Index (PMI) from Markit for manufacturing and services on Friday

Technical update. The S&P 500 Index came within 1.1% of a new record high last week, but ultimately it faltered late in the week and closed higher by just 0.2%. Markets are higher in early trading today and will once again look to make a run at the September 2 high point of 3588, while maintaining technical support at 3425.

COVID-19 news. New case growth decelerated in the United States over the weekend, taking the increase in the seven-day average down slightly to about 12% and near 55,000 daily new cases (source: COVID Tracking Project). Hospitalization growth slowed over the weekend as well, but the seven-day average still rose 25% week over week. France and Italy set new case records, while the United Kingdom may be headed for a national lockdown.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data are from FactSet and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking 1-05068721